CFIUS 2.0: Treasury Unveils Final Regulations to Govern Expanded Foreign Investment Screening

The final regulations are the culmination of a lengthy rulemaking process that kicked off in August 2018, when FIRRMA was enacted. As explained in our previous alert, FIRRMA represented the most sweeping overhaul of the operations and jurisdiction of CFIUS in its 45-year history. Likewise, the final regulations expand CFIUS’s jurisdiction and introduce new levels of complexity and nuance that require extensive regulatory analysis for investors and US target companies alike. The final rules are divided into two separate regulations – the first dealing with regular investments and the second dealing with just real estate transactions.

While a comprehensive treatise on the 327-page final CFIUS regulations will be of interest to many readers who have insomnia, we have instead chosen to highlight five areas and themes of the new CFIUS regulation covering regular investments. A separate alert will address the final regulations on real estate transactions.

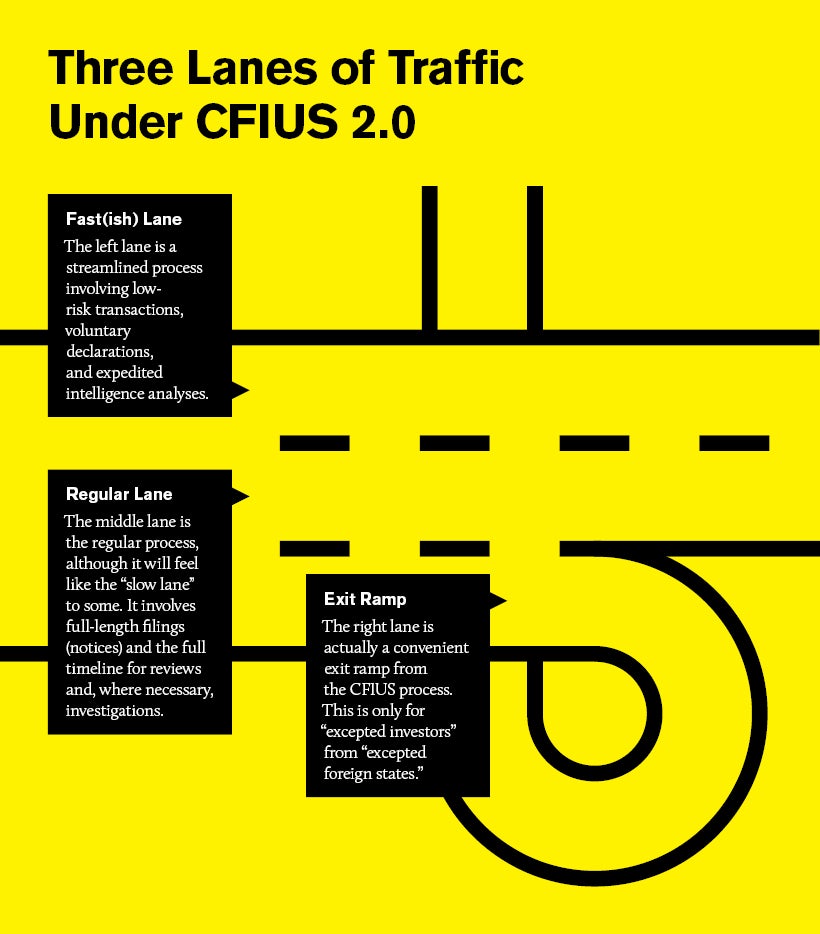

CFIUS: A Three-Lane Highway

With the final regulations, the Treasury Department essentially implemented a three-lane system for CFIUS reviews, just as Congress intended when it passed FIRRMA.

Regular Lane – Notices and Traditional CFIUS Reviews

The regular lane will utilize CFIUS’s traditional full-length filings, which are known as “notices,” and will need the full timeline for CFIUS review. However, this may feel like the slow lane to transaction parties in deals that are more complex or where CFIUS has questions because these types of reviews will still likely take several months.

For transactions filed using notices, the final regulations provide for an initial 45-day national security review, which includes a robust 20-day intelligence analysis by the US Intelligence Community, known as a “National Security Threat Assessment” (NSTA). The second stage, when needed, is a 45-day national security investigation with the option for CFIUS to grant itself a 15-day extension in “extraordinary circumstances” (such extensions are expected to be rare). The final stage is a 15-day window for the presidential determination. Therefore, where CFIUS seeks adverse action (by the President) against a transaction, the process for full filings can take 105 days, assuming no “extraordinary circumstances” would trigger an extension.

We summarize the types of transactions that require mandatory filings below, but it is worth noting that transactions of this nature may end up in the regular lane for reasons we will explain.

Fast(ish) Lane – Voluntary Declarations and Low-Risk Deals

The fast lane is the streamlined process that Congress provided for in FIRRMA when it created short-form filings known as “declarations.” It will involve low-risk transactions, voluntary declarations, and an expedited, simplified intelligence assessment known as “Basic Threat Information,” which Congress authorized CFIUS to use at its discretion in lieu of the traditional, more robust NSTA.

For transactions submitted as declarations, CFIUS will have a 30-day review period. Declarations were introduced in FIRRMA, and either a declaration or a joint voluntary notice (JVN) may be used to satisfy a mandatory declaration requirement. Declarations will be short in length (about five pages) and submitted on a standard fillable form. Under FIRRMA, CFIUS may respond to declarations in several ways and is not required to make a final determination on the basis of a declaration.

Exit Lane – “Excepted Investors” from “Excepted Foreign States”

This lane leads to a convenient exit ramp from the CFIUS process. It is available to “excepted investors” that meet a very narrow definition under the new CFIUS regulations. Of course, a central part of that definition involves excepted foreign states. The Treasury Department has selected Australia, Canada, and the United Kingdom as the initial excepted foreign states. The determination of which countries will qualify in the future as an “excepted foreign state” is based on a determination by CFIUS that the country has in place an effective, robust process for screening foreign investments for national security risks and coordinating with the United States on related matters. The three initial excepted foreign states are all members of the so-called “Five Eyes” intelligence partners and have a demonstrated history of cooperation and coordination with the United States on national security matters.

Excepted investors are low-risk foreign persons who will be exempt from CFIUS reviews for non-passive, non-controlling minority-investments and real estate transactions (but not for “control” transactions). The concept of “excepted investors” will be based on not just the foreign person’s connections to an excepted foreign state, but also the foreign person’s compliance with certain US laws, regulations, and other rules.

An investor interested in qualifying as an “excepted investor” must self-classify as one, based on its own determination that it meets the criteria set out in the final regulations. In order to be an excepted investor, the investor must meet one of the following definitions:

- A foreign individual who is a national of an excepted foreign state (and not also a dual-national of any foreign state that is not excepted);

- A foreign government of an excepted foreign state; or

- A foreign entity that meets each of five very specific criteria with respect to itself and each of its parents (if any).

The “excepted investor” concept will result in two de-facto tiers of foreign investors: those who are seen as inherently low-risk and meet the criteria, and everyone else. However, the definition of excepted investor is quite narrow, reflecting CFIUS’s concern over the growing complexity of ownership structures and its desire to prevent the circumvention of its jurisdiction (which was also a primary motivation of the US Senators who originally authored FIRRMA).

Two Types of Filings: Mandatory and Voluntary

When Are Mandatory Filings Required?

The final regulations implement FIRRMA’s provisions on mandatory and voluntary filings, which were among the law’s more significant changes to the CFIUS process. Stakeholders should be aware that, although we summarize the filing requirements below, the final CFIUS regulations are complex, and this summary is not intended to capture all of the requirements of the final rules comprehensively. Experienced CFIUS counsel should analyze whether a certain transaction requires a filing.

Transaction parties will be required to file a mandatory declaration (or notice) for certain transactions:

- involving “critical technology”; and

- where a foreign person acquires a “substantial interest” in a critical technology, critical infrastructure, or sensitive personal data (TID) US business, and a foreign government has a “substantial interest” in that foreign person.

As explained below, the Treasury Department incorporated the key elements of the 2018 critical technologies pilot program into the final regulations. If a transaction could result either in foreign control of a US business that “produces, designs, tests, manufactures, fabricates, or develops” a critical technology that is used in one of 27 sensitive industries (listed in an appendix to the regulations), or it constitutes a non-passive, non-controlling minority investment in such a US business, then the transaction parties must submit a mandatory filing.

The final CFIUS regulations do not contain an actual list of the critical technologies, because the universe of critical technologies is dictated by the lists of export-controlled technologies overseen by the Commerce and State Departments, and export controls are not static. Further, the Export Control Reform Act of 2018 (ECRA), which was enacted alongside FIRRMA as “sidecar” legislation, requires Commerce to examine and control “emerging” and “foundational” technologies that are “essential” to US national security, but neither of these categories have been fleshed out yet. Anything added by Commerce under that framework will also become a critical technology for CFIUS purposes, so stakeholders would be well-advised to monitor the potential expansion of export controls for emerging and foundational technologies.

Although the filing of a declaration will satisfy transaction parties’ mandatory filing obligation, in some instances (e.g., transactions involving a critical technology that the US Government considers especially sensitive), it may be advisable and ultimately more efficient to file a joint voluntary notice (JVN) instead of a declaration. Stakeholders will want a final determination from CFIUS (i.e., “safe harbor” from CFIUS taking adverse action in the future against a transaction that never underwent CFIUS review) yet, under the final regulations, they are only entitled to an “up or down” decision from CFIUS if they file a JVN. The filing of a declaration does not obligate CFIUS to make an actual decision regarding a transaction, which can be a source of frustration, delay, and expense for transaction parties.

Mandatory declarations must be submitted 30 days before the completion date of the transaction (for deals completed after March 14, 2020).

Voluntary Filings

CFIUS remains a largely voluntary process under the updated statute and regulations. The final regulations give substance to FIRRMA’s tight focus on critical technologies, critical infrastructure, and the sensitive personal data of US citizens. TID businesses are not subject to mandatory filing requirements unless the transaction meets the criteria laid out above. Rather, transaction parties can voluntarily file a declaration or JVN depending on the nature of the transaction.

As explained in our previous alert, non-passive, non-controlling minority investments in TID US businesses will typically be venture capital and other private equity investments through which a foreign person could obtain certain types of governance or information rights in the TID US business, including board membership or observer status (or the right to nominate someone to the board); access to the businesses’ “material nonpublic technical information”; or involvement in the company’s “substantive decision making” on critical technology, critical infrastructure, or sensitive personal data (other than through shareholder voting).

Critical Technologies, Critical Infrastructure, and Sensitive Personal Data

Deals Involving Critical Technologies

As noted, per FIRRMA and the new CFIUS regulations, critical technologies are comprised of not only items on the US Munitions List (USML) and certain items on the Commerce Control List (CCL), but also emerging and foundational technologies identified and controlled pursuant to ECRA.

Progress on new controls on emerging and foundational technologies has been slow. On January 6, 2020, Commerce issued an interim final rule adding software specially designed to automate the analysis of geospatial imagery to the Commerce Control List, restricting its export to all countries except Canada. Consequently, as explained in our alert discussing the implications of the interim rule, this software is now a “critical technology” under CFIUS regulations, and companies that “produce, design, test, manufacture, fabricate, or develop” such software may have to submit a CFIUS filing. Before that development, Commerce’s last action had been in November 2018, when it issued an Advanced Notice of Proposed Rulemaking (ANPRM) asking for public input on identifying “emerging technologies.” Moving forward, we expect that Commerce will issue controls on additional emerging technologies, as well as an ANPRM on foundational technologies to gather public and industry input.

In terms of how the CFIUS rules apply here, companies that “produce, design, test, manufacture, fabricate, or develop” critical technology may trigger a mandatory filing requirement or decide to do a voluntary filing for several reasons discussed below. Additionally, it is critical to note that companies that use a critical technology but do not engage in any of the above-listed activities will not be caught by the CFIUS regulations pertaining to non-passive, non-controlling minority investments involving critical technology. That being said, the activities that may trigger CFIUS jurisdiction – producing, designing, testing, fabricating, and developing – are not defined in the CFIUS regulations.

Ultimately, for US companies and investors, any new export controls on emerging and foundational technologies may result in CFIUS asserting jurisdiction for transactions not previously required to undergo CFIUS review. Further, because the imposition of export controls on emerging and foundational is an ongoing process, both companies and investors should be on the lookout for changes.

Mandatory Filings for Critical Technology Deals

In the final regulations, the Treasury Department incorporated the separate critical technologies pilot program it had implemented for non-controlling and controlling investments involving “critical technology” into the CFIUS regulations. If the transaction could result in foreign control of a US business that “produces, designs, tests, manufactures, fabricates, or develops critical technologies” used in one of the industries the Treasury Department has listed in an appendix, then a mandatory filing will be required.

For now, the Treasury Department will continue to use the same North American Industry Classification System (NAICS) codes that it used in the pilot program, enumerating 27 sensitive industries that will be covered by the mandatory filing requirement for critical technology. However, in the final regulations, the Treasury Department announced that it will issue a future notice of proposed rulemaking on this, departing from this industry-based approach for mandatory filing requirements. CFIUS will instead use “export control licensing requirements” to determine whether a critical technology transaction belongs to an industry that will be subject to mandatory filing requirements.

While it is unclear what the Treasury Department means by “export control licensing requirements,” it is possible that the Treasury Department will link mandatory filing for critical technology transactions to whether the technology at issue would require an export license if exported, reexported, transferred, or released to the country of the foreign investor. The Treasury Department will likely issue interim rules on this issue before February 13, 2020, creating additional anticipation for stakeholders.

Voluntary Filings for Critical Technology Deals

Non-passive, non-controlling minority investments in US companies that produce, design, test, manufacture, fabricate, or develop one or more “critical technologies” are now under CFIUS jurisdiction. However, if the investment (1) does not meet the criteria of the mandatory critical technology filings and (2) the foreign acquirer is not a foreign government, then notification of the transaction is purely voluntary and should be based on an evaluation of whether CFIUS might have concerns about the transaction’s national security risks. Experienced CFIUS counsel can assist with such an evaluation and advise on whether a filing would be prudent.

Deals Involving Critical Infrastructure

The final regulations expand CFIUS’s jurisdiction to include certain non-passive, non-controlling minority investments by a foreign person in a US company that “owns, operates, manufactures, supplies, or services critical infrastructure.” Treasury enumerated the specific critical infrastructure that can trigger this new area of CFIUS jurisdiction, listing 28 specific types of systems and assets within various infrastructure subsectors, such as telecommunications, utilities, energy, transportation, and manufacturing.

Deals Involving Sensitive Personal Data

The final regulations implement CFIUS’s jurisdiction over 11 specific categories of sensitive personal data, including financial, geolocation, health, biometric, and security clearance data, as well as electronic communications such as emails, text messages, and chat. These constitute sensitive personal data only if the US company:

- Targets or tailors its products or services to sensitive US Government personnel or contractors;

- Maintains or collects such data on greater than one million individuals; or

- Has a demonstrated objective to maintain or collect such data on greater than one million individuals, and such data is an integrated part of the US business’s primary products or services.

In the final regulations, Treasury Department also narrowed the scope of genetic information that would have been subject to CFIUS jurisdiction (under its original proposed draft regulations) to only results of an individual’s genetic tests whenever such results constitute identifiable data. “Genetic tests” is defined in reference to the Genetic Information Non-Discrimination Act of 2008 (42 U.S.C. 300gg-91(d)(17)). So, genetic testing data covered by CFIUS will not include genetic testing data derived from databases maintained by the US Government and routinely provided to private parties for research.

Foreign Limited Partners in Investment Funds

The final regulations also provide a special clarification for limited partners (LPs) who are foreign persons, have passive investments in a TID US business through an investment fund, and serve on that fund’s special advisory board or committee. This provision is derived from a very specific section of FIRRMA. Under the final rule, an investment can avoid being swept up by CFIUS jurisdiction if a series of specific criteria are met, such as the fund being managed by a general partner who is not a foreign person, the advisory board lacking the ability to impact investment decisions, and the passive foreign LPs lacking the ability to control the fund.

CFIUS will apply this exemption narrowly only to truly passive investors, and therefore it is in the best interests of investment funds to ensure that any foreign LPs do not have an active role in the management of the fund. As a result, stakeholders should clearly define roles for foreign LPs to avoid the entire fund being classified as a foreign person for CFIUS purposes.

A Notable Change from September’s Proposed Draft

Lastly, in the final regulations, the Treasury Department defined a new term, “principal place of business,” which has been a longtime element of the definition of “foreign entity.” Treasury is now seeking comments on the definition of “principal place of business,” which are due February 17, 2020. The final regulations define “foreign entity” as any entity “organized under the laws of a foreign state if either its place of business is outside the United States or its equity securities are primarily traded on one or more foreign exchanges.” The final regulations define “principal place of business” as “the primary location where an entity’s management directs, controls, or coordinates the entity’s activities, or in the case of an investment fund, where the fund’s activities and investments are primarily directed, controlled, or coordinated by or on behalf of the general partners, managing member, or equivalent.”

The impact of this new term may be that some investors who previously could have been categorized as a foreign entity will now be off the hook, under certain circumstances. Stakeholders should be aware that the final regulations tie the principal place of business of an entity to the most recent submission or filing to the US government or any foreign government.

- Related Industries

- Related Practices